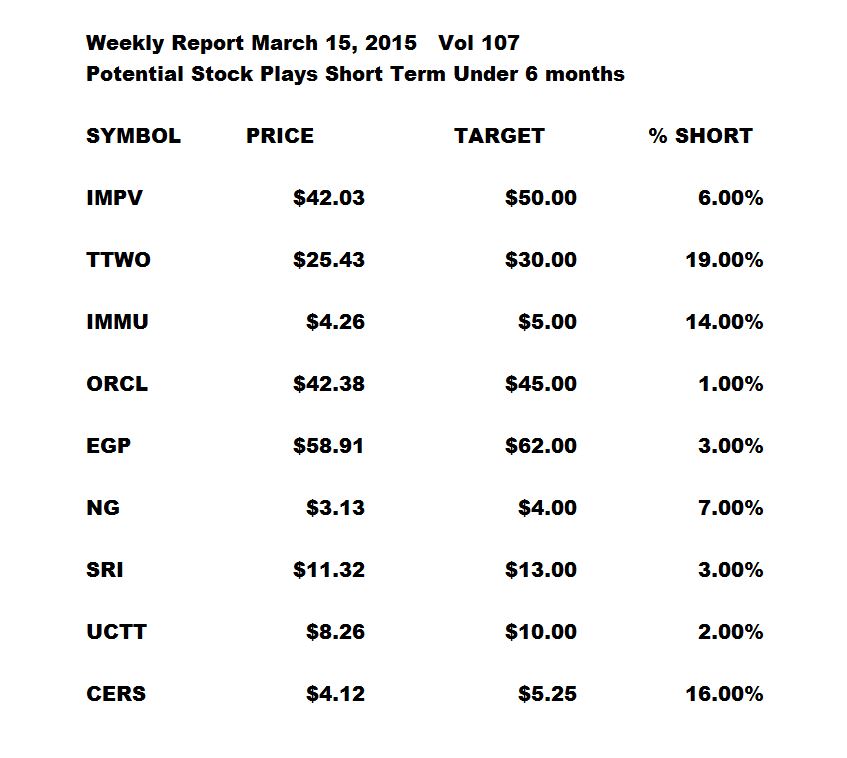

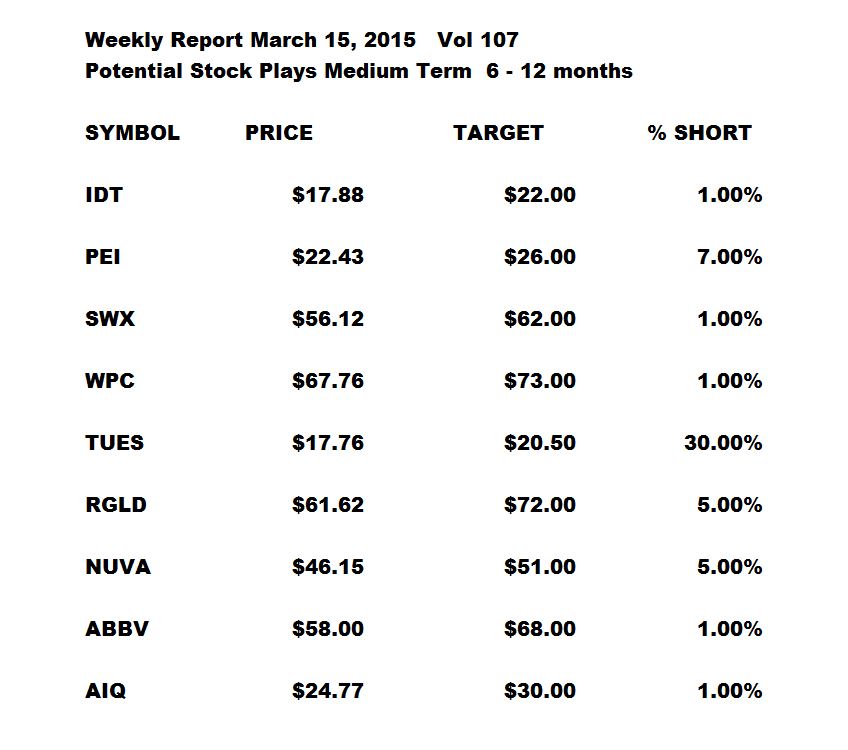

March 15, 2015 Vol. 107

Week in Review

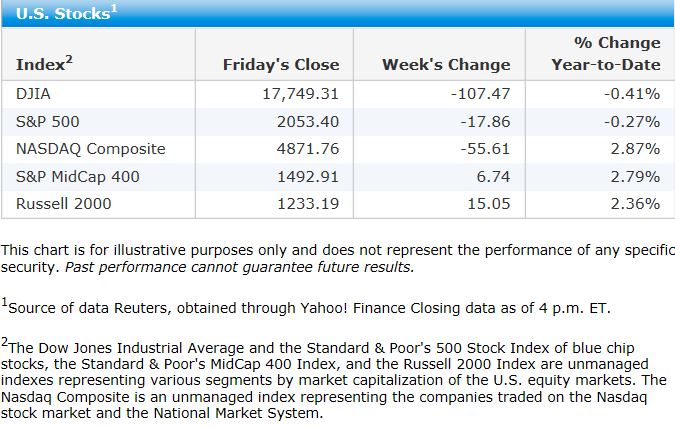

Stocks endure third weekly loss but remain near all-time highs Stocks ended lower after a volatile week of trading. The large-cap benchmarks endured a third consecutive week of losses, although they remained within a few percentage points of the all-time highs they established at the start of the previous week. The smaller-cap indexes fared better and even posted modest gains for the week. Small-cap stocks typically have less exposure to currency fluctuations, which many observers suggested as a large factor in the week’s selling.

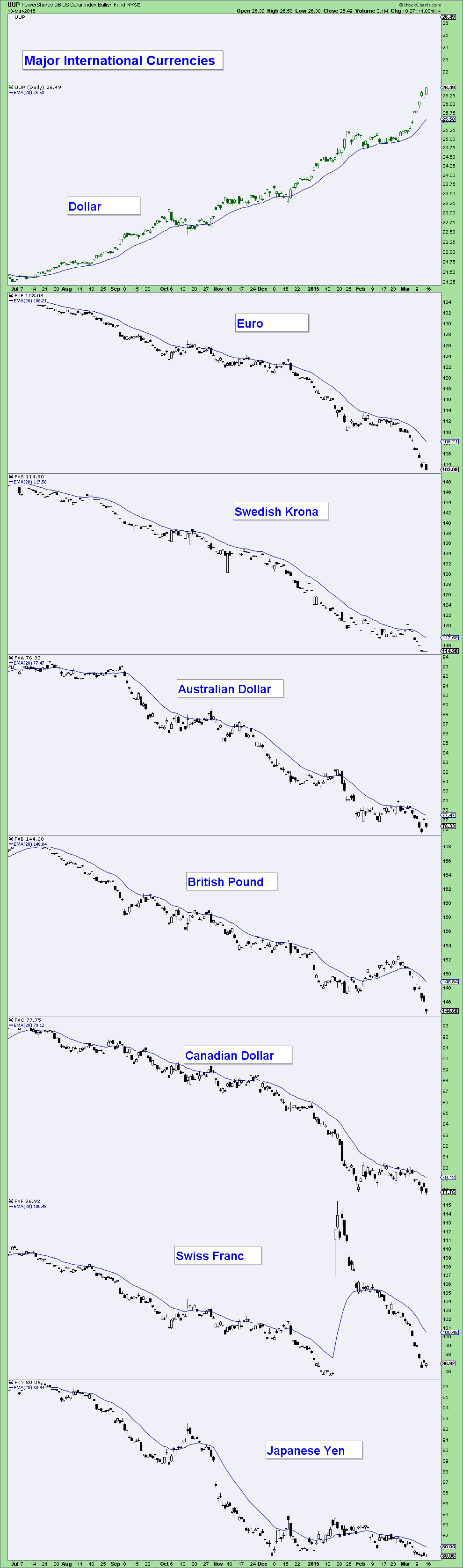

Investors worry about U.S. dollar strength With the fourth-quarter earnings season largely completed, it seemed clear that broader economic concerns were playing an important role in driving the market’s significant fluctuations during the week. The ongoing strength in the U.S. dollar appeared to weigh on sentiment as the greenback reached its highest level against a basket of other currencies in over a decade. The euro was a source of particular concern, as the beginning of a new bond buying stimulus program by the European Central Bank drove the currency still lower. U.S. corporations are experiencing a decline in the value of profits earned in Europe, while also seeing the costs of goods produced in the U.S. rise. Bad news for U.S. corporations is good news for their European competitors, however, and most major European exchanges closed higher for the week.

Weak retail sales may prove temporary Investors also seemed to be paying close attention to economic data that might cause Federal Reserve policymakers to signal an upcoming change in monetary policy following their meeting next week, even if the central bank is unlikely to announce any immediate increase in short-term interest rates. The week’s economic figures provided mixed signals in this regard, although none was as significant as the healthy monthly payrolls gain that drove the sell-off on March 6. On Thursday, stocks rallied after the government reported a surprising decline in retail sales in February, which some interpreted as a signal that might stay the Fed’s hand. Economists note that the retail sales pullback was sharply at odds with recent solid gains in labor income and that the harsh winter weather may have played a role, as it did last year. They anticipate that spending will recover in the coming months.

Consumers less confident despite wage and job gains Investors appeared to concentrate on the downside of weak economic data on Friday. Stocks opened mixed but then declined after the University of Michigan and Reuters reported that their gauge of consumer sentiment had declined to its lowest level since November. Confidence levels remained generally elevated, however, and some speculated that the poor weather, renewed market volatility, and a recent rise in gas prices might have temporarily weighed on consumer attitudes.

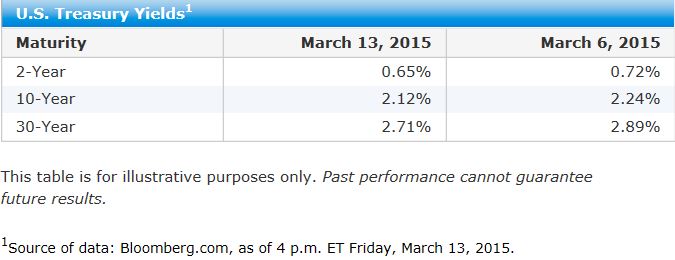

ECB bond buying pushes eurozone yields lower, benefiting Treasuries U.S. Treasury bonds rallied and recovered some of the ground that they lost last week, as the yield on the benchmark 10-year Treasury note decreased to 2.12%. (Bond prices and yields move in opposite directions.) The European Central Bank started buying eurozone sovereign bonds, pushing their yields to extremely low-or even negative-levels, which helped increase demand for relatively high-yielding U.S. Treasuries. Yields on German government debt are below 0.00% for maturities up to eight years. A weaker-than-expected February U.S. retail sales report also helped support Treasury prices.

Investment-grade corporates digest heavy new issuance The primary market for investment-grade corporate bonds continued to boom as investors eagerly digested a heavy volume of new issuance. However, the supply weighed on the secondary market to some degree. High yield corporate bonds experienced selling pressure amid large outflows from high yield exchange-traded funds as well as heightened equity market volatility. Expectations for robust new issuance also dampened demand for high yield bonds.

Positive returns for broad municipal bond market Municipal bonds generated positive returns despite the heaviest weekly new issuance since December 2014. Approximately $12 billion of new municipal bonds came to market, led by a large new deal from the University of California. Investor demand for the supply reaching the market was generally strong. Municipal debt prices, which tend to track trends in the Treasury market, also benefited from the rally in Treasuries.

Brazilian currency continues to fall Brazil continued to dominate the headlines in emerging markets. The country’s currency, the real, fell further against the U.S. dollar and has now lost about 15% for the year to date. However, minutes from the Central Bank of Brazil’s most recent policy committee meeting gave no indication that the bank will accelerate the pace of rate increases to support the currency or contain inflation, pointing to a 50-basis-point hike in April. (A basis point is 0.01 percentage points.)

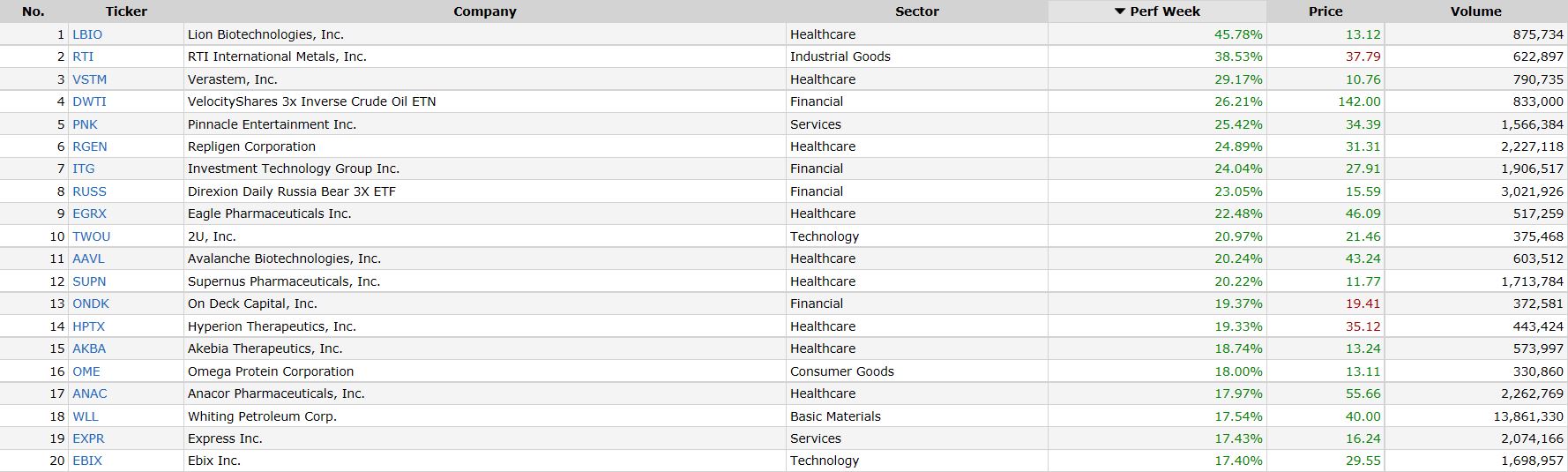

Weekly Gainers %

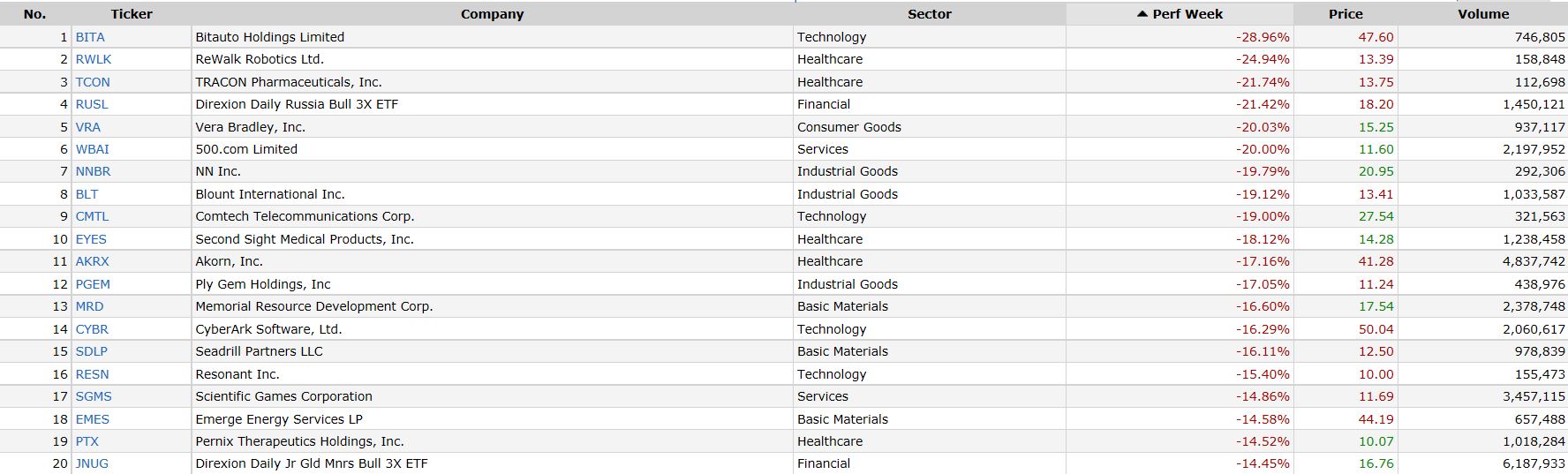

Weekly Losers %

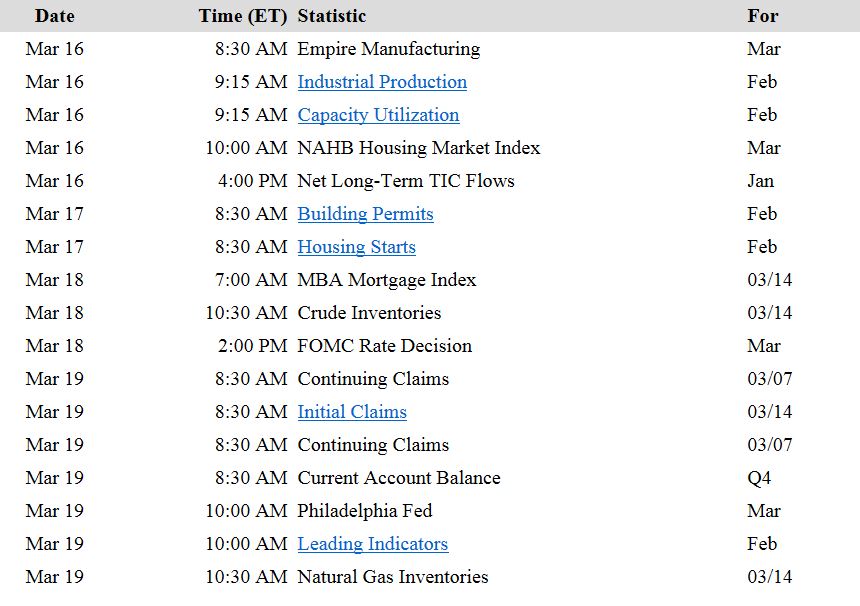

Economic Events

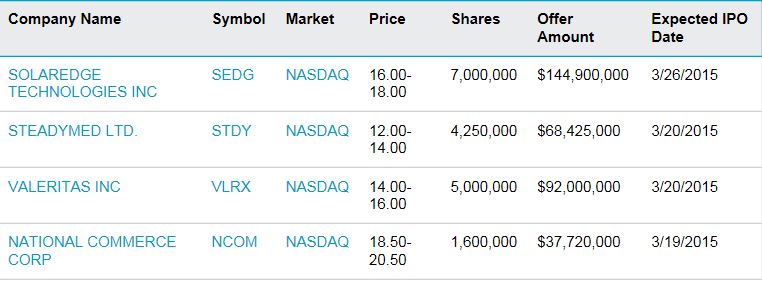

Upcoming IPO’s

This week’s notable earnings with a Float minimum of 10%

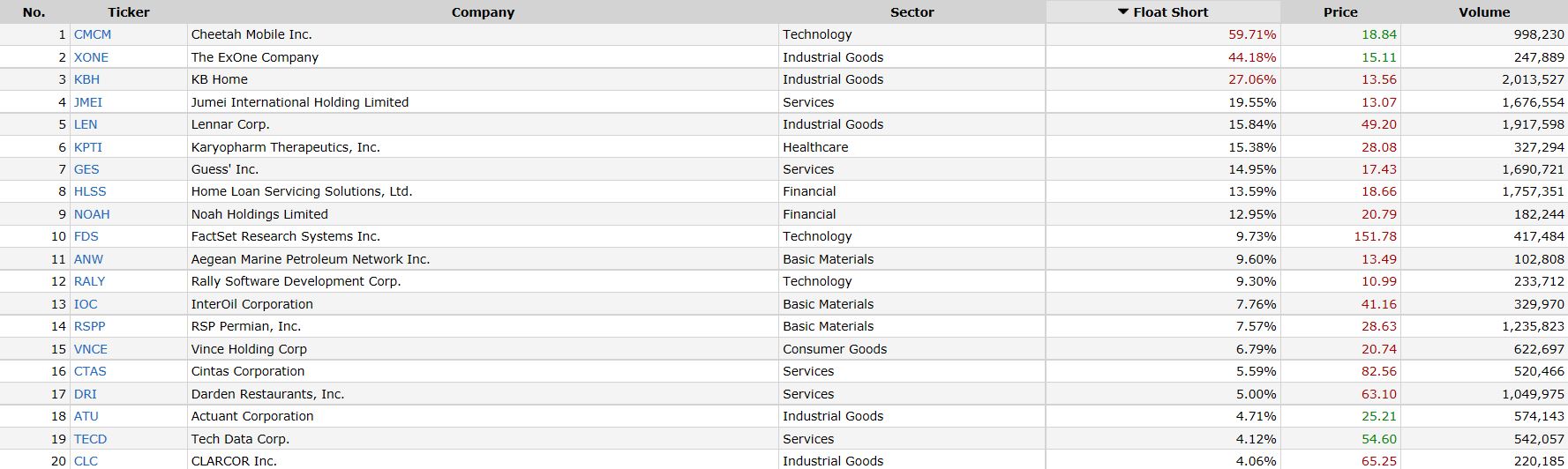

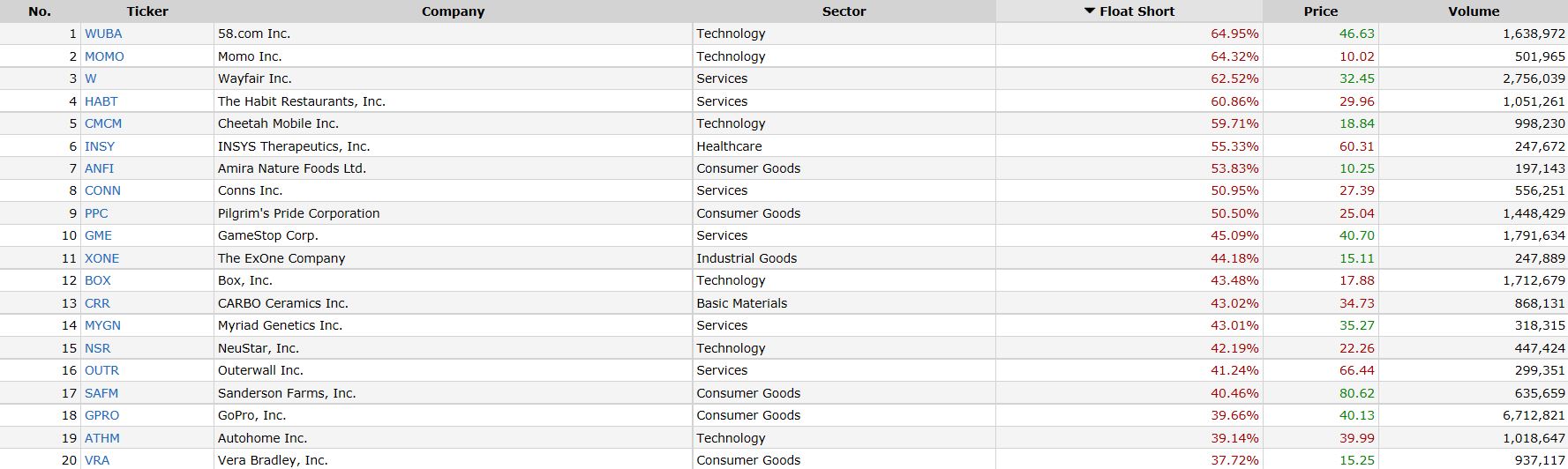

Top 20 Percentage Float Short

Currencies

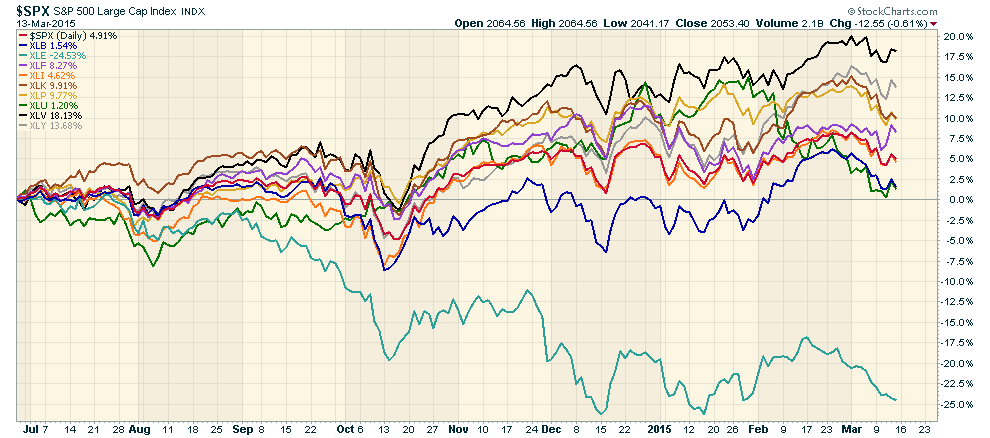

Sectors

The Financial Sector leads the way for the week

Industry Charts

The top Industry in the Health Care Sector for the week was $DJUSHP…Health Care Providers

A chart to watch in the above Industry…AIQ

To receive this weekly report and daily market videos, SMS trade or investment alerts Private chat and so much more for you to build your portfolio.

Matt Cowell is an Investment Analyst for Facultas Capital Management and has outperformed the market for many years using technical analysis. His team at Milestone Capital Growth Portfolio is committed to producing the best options for their members.

To join the Private Club at Milestone Click Here http://milestonecapitalgrowthportfolio.com/join-us/

We will see you on the other side.

http://milestonecapitalgrowthportfolio.com/ , its affiliates and partners, shall have no liability for investment or other decisions based upon any Content and/or decisions based upon a contrarian view of any Content. The Content is to be used for informational and entertainment purposes only and we cannot provide investment advice for any individual. We advise that you contact your personal broker before making any investment related to any information received from the Site. http://milestonecapitalgrowthportfolio.com/ , its affiliates and partners specifically disclaim any and all liability or loss arising out of any action taken in reliance on Content, including but not limited to market value or other loss on the sale or purchase of any company, property, product, service, security, instrument, or any other matter.

More Information http://milestonecapitalgrowthportfolio.com/terms-conditions-of-use/

Team”MCGP”

{kind=link}